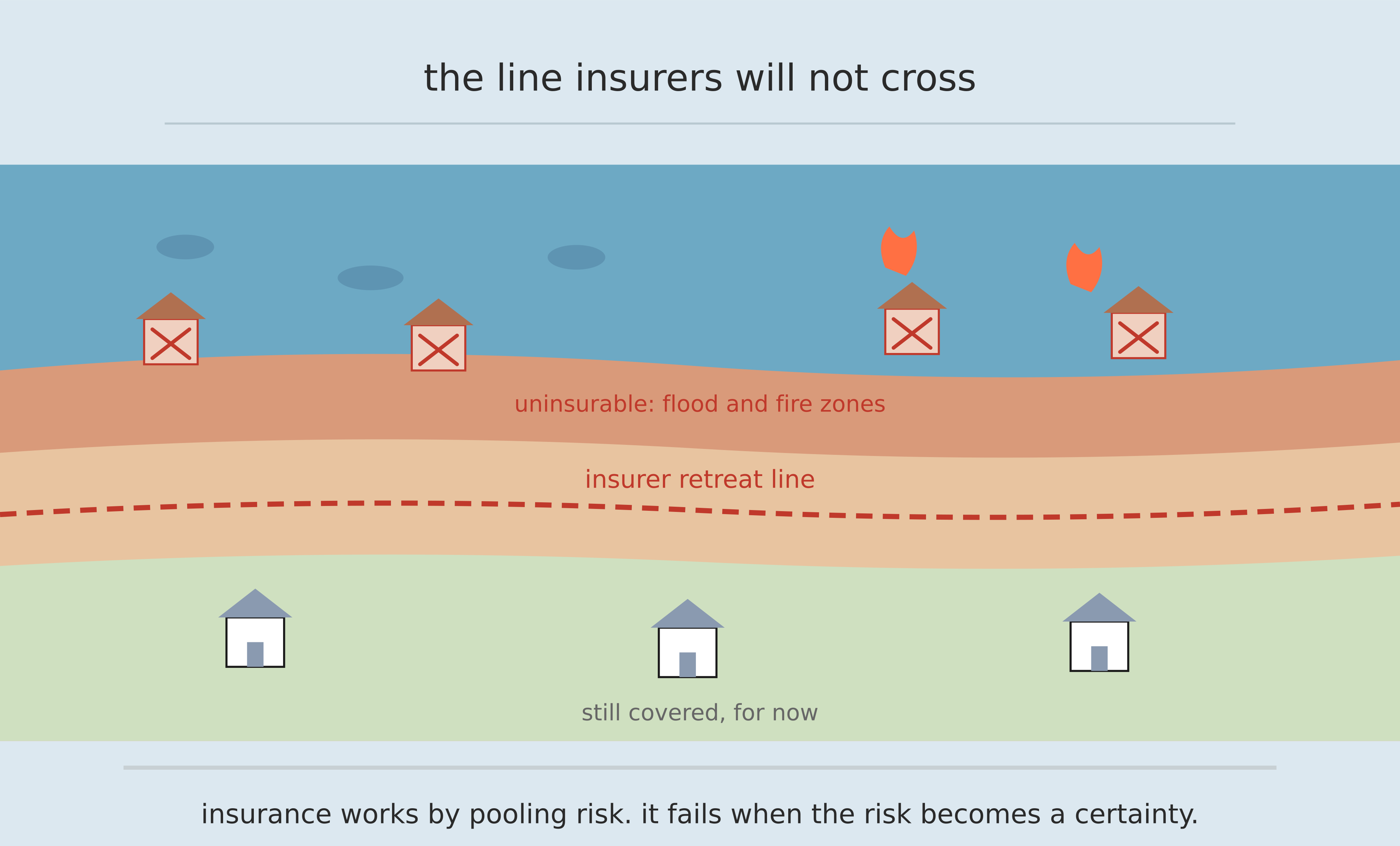

The insurance industry is built on a mathematical premise: individual risks, pooled across enough people, become statistically predictable. A single house fire is unpredictable. A million house fires across a portfolio are not. The insurer charges premiums calibrated to the expected loss, adds a margin for profit and administrative cost, and the system functions as long as the risks in the pool are diverse enough that catastrophes do not strike everyone simultaneously.

Climate change is breaking this premise. Not by making individual risks unpredictable, but by making them correlated. When a major hurricane hits Florida, it does not hit one house. It hits hundreds of thousands of houses at the same time, in the same geography, insured by the same regional carriers. When a wildfire burns through a California county, it does not claim one policy. It claims thousands in a single event. The diversification that makes insurance mathematically viable is being eroded by the increasing frequency and intensity of correlated climate events.

The Retreat Already Happening

This is not a future scenario. It is a present one. State Farm and Allstate stopped writing new homeowners policies in California in 2023. Multiple major insurers have withdrawn from Florida, where the combination of hurricane exposure and sea-level rise has made actuarial viability impossible at premiums that homeowners can pay. AXA has withdrawn from certain coastal markets in France. Insurers across Australia have been raising premiums for flood-exposed properties to levels that have effectively made coverage inaccessible to the people who most need it.

The withdrawal is proceeding faster than most people recognize because it happens incrementally: a carrier stops writing new policies here, raises premiums to unaffordable levels there, excludes specific perils in specific geographies through policy language that most policyholders do not read until they try to make a claim.

The result is a growing population of properties that are technically insurable but practically uninsured, because the premiums required to cover the actual risk exceed the financial capacity of the owners.

What Uninsurability Actually Means

Insurance is not a luxury. In most wealthy countries, mortgage lenders require homeowners insurance as a condition of the loan. A property that cannot obtain insurance cannot obtain a mortgage. A property that cannot obtain a mortgage cannot be sold at conventional market prices. An uninsurable property is, in practical terms, an asset that cannot be transferred, financed, or rebuilt after a loss.

The communities facing this crisis first are not, in general, the wealthiest ones. They are coastal communities with high flood exposure, mountain communities in fire-prone landscapes, agricultural regions facing extreme weather events. Many of these communities have existed in their current locations for generations. The value of their properties, the collateral for their mortgages, the foundation of their retirement savings, is being destroyed not by the climate events themselves but by the withdrawal of the financial infrastructure that made those properties viable assets.

The Public Insurer of Last Resort

When private markets fail to provide essential services, governments face a choice: subsidize the private market back into operation, provide the service directly, or leave the gap unfilled. For insurance, most wealthy governments have chosen the first option. State-backed insurers of last resort, the Citizens Property Insurance Corporation in Florida, the California FAIR Plan, the National Flood Insurance Program in the United States, have been created to provide coverage that private markets refuse to offer. They are chronically underfunded, politically contentious, and structurally set up to subsidize development in exactly the high-risk locations where development is most dangerous.

The deeper question is whether the insurer of last resort model is a sustainable response to a risk environment that is systematically moving beyond the capacity of actuarial pooling. Or whether it is a mechanism for delaying, at public expense, the geographical reckoning that climate change is forcing: the acknowledgment that some places, built in some ways, cannot be made safe at the cost their current inhabitants can bear.

Insurance is not just a financial product. It is the mechanism by which societies decide which risks are acceptable and which are not. The places where insurance is becoming impossible are, in a real sense, the places where the answer to that question is being rendered by the market rather than by any deliberate collective decision.

Leave a comment